Introduction

Financial institutions sit at the intersection of two things attackers want most: money and data. Every day, Visa's network alone processes roughly 639 million transactions — and behind each transaction sits a record containing account credentials, Social Security numbers, or card details.

The cost of failing to protect that data is steep. According to IBM's Cost of a Data Breach Report, the average financial sector breach cost $6.08 million in 2024 — well above the global average of $4.88 million across all industries.

This article breaks down what you need to know:

- What financial services cybersecurity means in practice

- The specific threats targeting this sector, with real attack examples

- Defensive solutions and the compliance frameworks that govern them

- Where the industry is heading next

Whether you're a security professional, compliance officer, or executive, you'll finish with a clear picture of the threat landscape and what to do about it.

TL;DR

- Financial sector breaches average $6.08M — nearly 25% above the global average

- The top threats: phishing/BEC, ransomware, DDoS, insider threats, and API/supply chain attacks

- MFA alone blocks 99.9% of automated credential attacks — yet many firms still haven't mandated it

- PCI DSS, GLBA, SOX, and NY DFS Part 500 each mandate specific security controls — penetration testing included

- AI-powered attacks and synthetic identity fraud are outpacing most institutions' ability to detect and respond

What Is Financial Services Cybersecurity?

Financial services cybersecurity is the practice of protecting banks, credit unions, investment firms, insurance companies, payment processors, and fintechs from unauthorized access, data theft, fraud, and disruption of their digital systems.

The Three Core Goals

Every security program in this sector must hit all three objectives at once:

- Confidentiality — protecting customer PII, account credentials, and financial records from unauthorized disclosure

- Integrity — preventing manipulation of transactions, account balances, or audit records

- Availability — keeping online banking portals, payment systems, and trading platforms operational

Why Financial Services Is Different

Financial institutions operate under a distinct set of pressures that most other industries simply don't face:

- Massive financial assets are directly accessible (not just records, but transferable funds)

- Regulatory mandates are specific, overlapping, and carry serious penalties for non-compliance

- Real-time transaction processing means security controls cannot introduce meaningful latency

- Interconnected systems mean a breach at one institution can cascade across the broader financial ecosystem

Together, these pressures mean a security program built for a generic enterprise won't hold up here. Financial institutions need controls designed around their specific risk profile, regulatory environment, and operational requirements.

Why Financial Institutions Are Prime Targets

The Verizon 2024 Data Breach Investigations Report documented 3,348 security incidents and 1,115 confirmed data breaches in the Finance and Insurance sector in a single year. 95% were financially motivated.

The calculus is straightforward for attackers: financial firms hold both money (directly transferable) and data (sellable on dark web markets). In 2024, 269 million card records and 1.9 million stolen bank checks appeared on dark and clear web platforms.

An Expanded Attack Surface

Traditional banking operated within a defined perimeter. Modern financial institutions look very different:

- Mobile apps accessible from any device, anywhere

- Cloud-hosted infrastructure spanning multiple providers

- Open banking APIs connecting dozens of third-party vendors

- Fintech partnerships that share data and system access

Each integration is a potential entry point. Digital transformation has delivered real value, but it's also multiplied the number of doors attackers can try.

Reputational and Operational Stakes

More attack surface means more consequence when something goes wrong. A breach at a financial institution erodes consumer trust fast — and in digital banking, lost trust rarely comes back. A single high-profile incident can push customers to competitors permanently.

The financial and operational fallout compounds that damage:

- Regulatory fines from bodies like the SEC, OCC, or state regulators

- Operational disruption from taking systems offline to contain an attack

- Ransom pressure created by the urgency to restore service quickly

That pressure to get back online is precisely why attackers expect financial firms to pay. Speed works against careful incident response.

Common Cyber Threats in Financial Services: Definitions and Real-World Examples

Phishing and Business Email Compromise (BEC)

Phishing in financial services targets more than just customers. Attackers impersonate regulators, executives, or trusted counterparties to extract credentials, authorize wire transfers, or deploy malware. Business Email Compromise is the high-stakes variant: attackers spoof or compromise executive email accounts, then instruct treasury or finance staff to move funds urgently.

The numbers are staggering. The FBI IC3 2024 Annual Report recorded nearly $2.8 billion in BEC losses in a single year — making it the second-costliest cybercrime category reported. Cumulative losses from 2022 through 2024 reached approximately $8.5 billion. The median fraudulent transaction: $50,000.

The attack pattern is consistent: urgent email from a spoofed CEO, instruction to wire funds to an unfamiliar account, pressure to bypass normal approval processes. Firms that combine staff training with mandatory out-of-band wire verification — a phone call to a known number, not a reply to the email — stop the majority of these attempts before funds move.

Ransomware and Malware

Ransomware in financial services doesn't just encrypt laptops. It targets core banking platforms, payment infrastructure, and customer databases — and modern variants use double extortion: exfiltrate data first, then encrypt, threatening public exposure if the ransom goes unpaid.

The November 2023 LockBit attack on ICBC Financial Services illustrated the systemic risk. Exploiting the Citrix Bleed vulnerability (CVE-2023-4966), attackers disrupted ICBC's role in the $26 trillion US Treasury market and temporarily left the firm owing BNY Mellon $9 billion — settled via USB stick-delivered trade confirmations.

Six months later, LockBit hit Evolve Bank & Trust after an employee clicked a malicious link. The breach exposed sensitive data for 7.6 million Americans and cascaded to fintech partners Wise and Affirm. Evolve refused to pay; LockBit leaked the data anyway.

Distributed Denial of Service (DDoS) Attacks

A DDoS attack floods a bank's online portal, payment gateway, or trading platform with illegitimate traffic until it collapses for legitimate users. Financial services is consistently among the primary targets — NETSCOUT's 1H 2024 threat intelligence report identified banking and financial services as a top DDoS target, with high-intensity attacks escalating beyond 100 Gbps.

DDoS attacks are often smokescreens. While IT teams scramble to restore availability, attackers may be attempting a secondary intrusion deeper in the network. Operation Ababil (2012–2013) targeted JPMorgan Chase, Bank of America, Citigroup, and Wells Fargo with sustained attacks attributed to state-aligned actors. More recently, the Killnet collective conducted DDoS campaigns against European banks throughout 2022–2023 in response to geopolitical events.

Insider Threats

Insider threats originate from people with legitimate access: employees, contractors, and third-party personnel who misuse that access — deliberately or accidentally. They're particularly dangerous because they use valid credentials and understand system architecture.

The Verizon 2024 DBIR found that 31% of Finance and Insurance sector breaches involved internal actors. Malicious insider incidents average $4.99 million per breach — higher than most external attack categories. In December 2024, former TD Bank teller Derek Aut was arrested for stealing more than $180,000 from customer accounts.

Accidental insider incidents are equally costly. A misconfigured cloud storage bucket, an over-permissioned API key left in code, or a contractor with excessive database access can expose millions of records with no malicious intent involved.

API and Third-Party Supply Chain Attacks

Open banking APIs and third-party integrations — payment processors, KYC vendors, cloud providers — introduce external code and trusted access pathways. If a vendor's software is compromised, attackers can move laterally through that trusted connection into the financial firm's core systems.

Two recent breaches show how quickly that trust becomes a liability:

- MOVEit / Nebraska bank (2023): Cl0p exploited a flaw in the MOVEit file transfer tool, resulting in a $2.4 million settlement for one Nebraska-based bank

- Evolve Bank supply chain cascade (2024): The LockBit breach at Evolve propagated directly to fintech partners Wise and Affirm, demonstrating how banking-as-a-service models create concentration risk

Third-party software vulnerabilities surged 68% in the 2024 Verizon DBIR compared to the prior year. The average organization now experiences 12 third-party breaches annually, according to Ponemon Institute research.

Essential Cybersecurity Solutions for Financial Institutions

Identity and Access Management (IAM) and MFA

IAM ensures only authorized users access specific systems — and Multi-Factor Authentication adds a second verification layer before granting that access. Microsoft's research found MFA-protected accounts are 99.9% less likely to be compromised. Google's study showed SMS-based MFA blocks 100% of automated bots and 96% of bulk phishing attacks.

For financial institutions, MFA should cover every privileged account, every customer-facing authentication point, and every administrative interface — without exception.

Web Application Firewalls, DDoS Protection, and API Security

- WAFs filter malicious web traffic, blocking SQL injection, cross-site scripting, and automated bot attacks before they reach application logic

- DDoS mitigation reroutes flood traffic to scrubbing centers, keeping portals and payment gateways available under attack

- API security gateways enforce authentication, rate limiting, and schema validation on all inter-system calls — critical for open banking environments

Advanced Threat Detection and Security Operations

Security Information and Event Management (SIEM), Endpoint Detection and Response (EDR), and AI/ML anomaly detection tools help security teams spot suspicious behavior before it becomes a breach. In financial services, detection speed directly limits loss — a wire transfer fraud caught at initiation is recoverable; one caught three days later often isn't.

Key indicators to monitor:

- Unusual login patterns and off-hours access

- Large or unexpected data transfers

- Lateral movement between systems

- Privilege escalation attempts

Vulnerability Assessment and Penetration Testing (VAPT)

VAPT is the practice of identifying and exploiting vulnerabilities before attackers do. The distinction between automated scanning and manual penetration testing matters enormously here.

Automated scanners detect known vulnerabilities efficiently, but they miss business logic flaws, complex attack chains, authorization gaps, and misconfigurations that require human reasoning to surface.

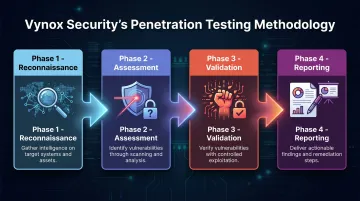

Vynox Security's manual-first penetration testing was built specifically to address this gap. Their four-phase methodology — Reconnaissance, Assessment, Validation, and Reporting — is structured to uncover what automated tools routinely leave behind:

- Reconnaissance — Asset discovery and threat modeling before testing begins

- Assessment — Expert-led manual testing of core banking systems, payment gateways, mobile apps, and APIs (aligned to OWASP Top 10, OWASP ASVS, OWASP API Security Top 10, and NIST guidelines)

- Validation — Proof-of-concept testing for every finding, eliminating false positives and confirming actual exploitability

- Reporting — Audit-ready reports mapped to PCI DSS, SOC 2, ISO 27001, and RBI requirements, with clear remediation guidance structured for both technical teams and executives

For financial institutions, Vynox Security specifically tests core banking applications, payment processing infrastructure, open banking APIs, mobile banking platforms, and third-party integrations — covering the full attack surface that compliance checklists routinely overlook.

Employee Security Awareness Training and Incident Response

Most successful attacks against financial institutions begin with a human: clicking a phishing link, misconfiguring a system, or falling for a pretexting call. Role-based training — particularly phishing simulations that reflect current attack techniques, including AI-generated content — is a foundational control that reduces initial compromise risk before technical defenses are even tested.

Pair training with a tested incident response plan that covers detection, containment, notification, and recovery. Regulatory notification windows are tight — the SEC's cybersecurity disclosure rule requires material incident disclosure within four business days — so teams that haven't run tabletop exercises will struggle to meet them under real pressure.

Cybersecurity Compliance Frameworks in Financial Services

US financial institutions operate under multiple overlapping regulatory frameworks:

| Framework | Core Requirement |

|---|---|

| PCI DSS 4.0 | Protects cardholder data; Requirement 11.4 mandates regular penetration testing |

| GLBA Safeguards Rule | Requires encryption, MFA, designated security personnel, and a comprehensive information security plan |

| SOX | Protects the integrity of financial reporting systems |

| NY DFS Part 500 | Requires formal cybersecurity programs, MFA, incident reporting within 24 hours for ransom payments |

| DORA (EU) | Effective January 2025; mandates ICT risk management, resilience testing, and third-party oversight |

Compliance frameworks establish a necessary baseline. They force institutions to implement encryption, access controls, security testing, and incident notification procedures. Meeting those requirements, however, doesn't guarantee protection. Sophisticated attackers don't design their methods around what auditors check.

Penetration Testing and Compliance

PCI DSS, SOC 2, and ISO 27001 all explicitly require regular security testing to validate that controls are functioning. For financial institutions maintaining these certifications, the testing must produce documented, audit-ready evidence — not just a scan summary.

Audit-ready penetration test reports typically include:

- Findings mapped to specific control requirements (e.g., PCI DSS Requirement 11.4)

- Proof-of-concept evidence for each confirmed vulnerability

- Risk-to-business-impact analysis, not just CVSS scores

- Remediation guidance auditors can trace through to closure

Vynox Security structures its reports to meet exactly these standards, with report delivery under 48 hours — a turnaround that fits most regulatory reporting timelines.

Emerging Cybersecurity Trends in Financial Services

AI on Both Sides of the Attack

Generative AI appeared in 16% of breaches tracked in IBM's 2025 Cost of a Data Breach Report, primarily scaling phishing and social engineering. AI-generated phishing messages are grammatically flawless, contextually personalized, and increasingly indistinguishable from legitimate communications.

On defense, AI/ML tools are improving anomaly detection, cutting false positive rates by 75–90%, and accelerating incident triage. Gartner projects that by 2027, 90% of successful AI implementations in cybersecurity will be tactical — focused on threat detection and alert management rather than strategic planning.

Deepfakes and Synthetic Identity Fraud

In early 2024, a finance employee at a Hong Kong multinational was deceived into transferring $25 million after fraudsters used deepfake technology to impersonate the company's CFO on a video conference call. The incident confirmed what security researchers had warned: voice and video deepfakes are active weapons — already deployed against real targets.

Synthetic identity fraud — combining real and fabricated data to create fraudulent identities — now accounts for up to 80% of new account fraud at financial institutions. US losses are estimated at $30–35 billion annually, with lender exposure reaching $3.3 billion in H1 2025 alone.

Zero Trust and Quantum Readiness

Zero Trust — verify every user, every device, at every access point — is replacing perimeter-based security as the architecture standard. A Gartner survey found 63% of organizations have fully or partially implemented a zero-trust strategy, though for most, it still covers less than half their environment. Financial services firms are accelerating adoption, driven by cloud migration and open banking requirements.

That same drive to future-proof infrastructure extends to cryptography. NIST released its first three finalized post-quantum encryption standards in August 2024 (FIPS 203, 204, and 205). The threat of quantum decryption isn't imminent, but "harvest now, decrypt later" attacks mean financial institutions protecting long-lived data need to begin transition planning today — migration timelines typically run 3–5 years, and most organizations are already behind.

Key steps for quantum readiness include:

- Inventory data assets by sensitivity and expected lifespan

- Identify cryptographic dependencies across systems and third-party vendors

- Pilot NIST-approved post-quantum algorithms in non-critical environments first

- Align timelines with regulatory guidance as it emerges

Frequently Asked Questions

What is financial cybersecurity?

Financial cybersecurity is the practice of protecting financial institutions — banks, credit unions, investment firms, fintechs, and payment processors — from cyber threats. The goal is preserving the confidentiality, integrity, and availability of financial services and the customer data they hold.

What are the cyber threats to financial services?

The primary threats are phishing and BEC, ransomware, DDoS attacks, insider threats, and API/supply chain attacks. Financial institutions hold high-value money and data — which is why they remain among the most targeted sectors globally.

How does cybersecurity apply to financial services?

It applies across every layer of financial operations:

- Protecting customer data and transactions

- Maintaining uninterrupted digital services

- Meeting regulatory compliance requirements

- Preventing financial fraud

- Preserving consumer trust in digital banking platforms

Every layer — from authentication to transaction monitoring to incident response — is part of the program.

What are the top 3 trends in the cybersecurity industry?

AI-powered attacks and defenses, the rise of Zero Trust Architecture as the dominant security model, and the growing threat of deepfakes and synthetic identity fraud. In financial services, all three directly threaten identity verification and transaction integrity — the two pillars institutions cannot afford to compromise.

What are the 5 C's of cybersecurity?

The 5 C's are:

- Change — adapting security controls as threats evolve

- Compliance — meeting regulatory mandates like PCI DSS, SOC 2, and GDPR

- Cost — balancing security investment against actual risk exposure

- Continuity — maintaining operational resilience when incidents occur

- Coverage — ensuring no systems or endpoints are left unprotected

For financial institutions, all five are in constant tension — which is why a structured security program matters more than point solutions.